Conversational AI in financial services is software that uses natural language processing, machine learning, and speech recognition to hold real, two-way conversations with banking customers across chat, voice, and mobile apps. It handles account questions, fraud alerts, loan pre-screening, and compliance disclosures inside one regulated interface, instead of routing every request to a human agent.

What is conversational AI in financial services?

Conversational AI in financial services is the layer of software that lets a bank, insurer, or fintech talk to customers in plain language and act on what those customers actually said. It combines natural language processing, large language models, retrieval over the institution's own data, and integrations into core banking systems so the conversation can move money, surface a statement, or open a dispute, not just answer FAQs.

It is not the same as a generic AI chatbot. A generic chatbot guesses an answer from public data. A financial services conversational AI agent works against authenticated customer records, sits behind the same audit and access controls as a human agent, and is bounded by what the regulator allows it to say about products, fees, and advice.

I've reviewed dozens of conversational AI rollouts in fintech and banking over the last three years, and the working ones share three traits. They are grounded in the institution's own knowledge base instead of the open web. They escalate to a human the moment confidence drops or a regulated topic comes up. And they log every exchange to the same case-management system the compliance team already audits.

The vocabulary matters here because buyers conflate three things. A rules-based chatbot follows a decision tree. A virtual assistant adds NLP on top so it can handle paraphrased questions. A conversational AI agent goes further, holds context across turns, calls tools and APIs to take action, and can hand off to a teammate without losing the thread. For a deeper walk-through with cross-industry comparisons, our roundup of conversational AI examples is a good companion read.

Why financial services need conversational AI in 2026

Customer expectations, support cost pressure, and regulator interest are all moving in the same direction at the same time, and conversational AI is sitting at the center of that overlap. Banks that wait another budget cycle are quietly handing share to digital-first competitors who already automated the boring 70% of their inbound queue.

Customers want answers in seconds, not the next business day, and they want them on whichever channel they already use, in-app chat, WhatsApp, voice, the mobile banking widget. According to PYMNTS, nearly three in four bank customers want greater personalization, and embedded conversational AI is the most realistic way to deliver it at scale without hiring a new tier of relationship managers.

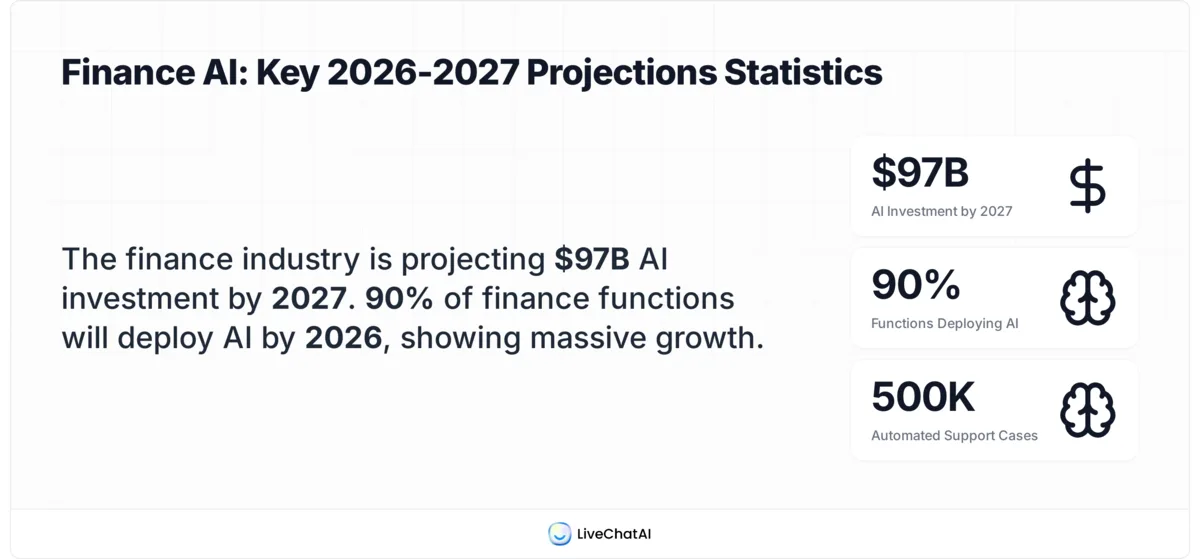

The cost case is just as direct. Front-line support is the second-largest operating expense at most retail banks after physical branches, and tier-one questions like "what's my balance" or "why was I charged this fee" still consume the majority of agent minutes. According to CGI, one international financial services firm now runs 500,000 customer support conversations per year through a single conversational AI deployment, cutting roughly 2 million euros of annual cost. If you want benchmarks for what your own queue could absorb, our breakdown of customer support cost walks through industry numbers.

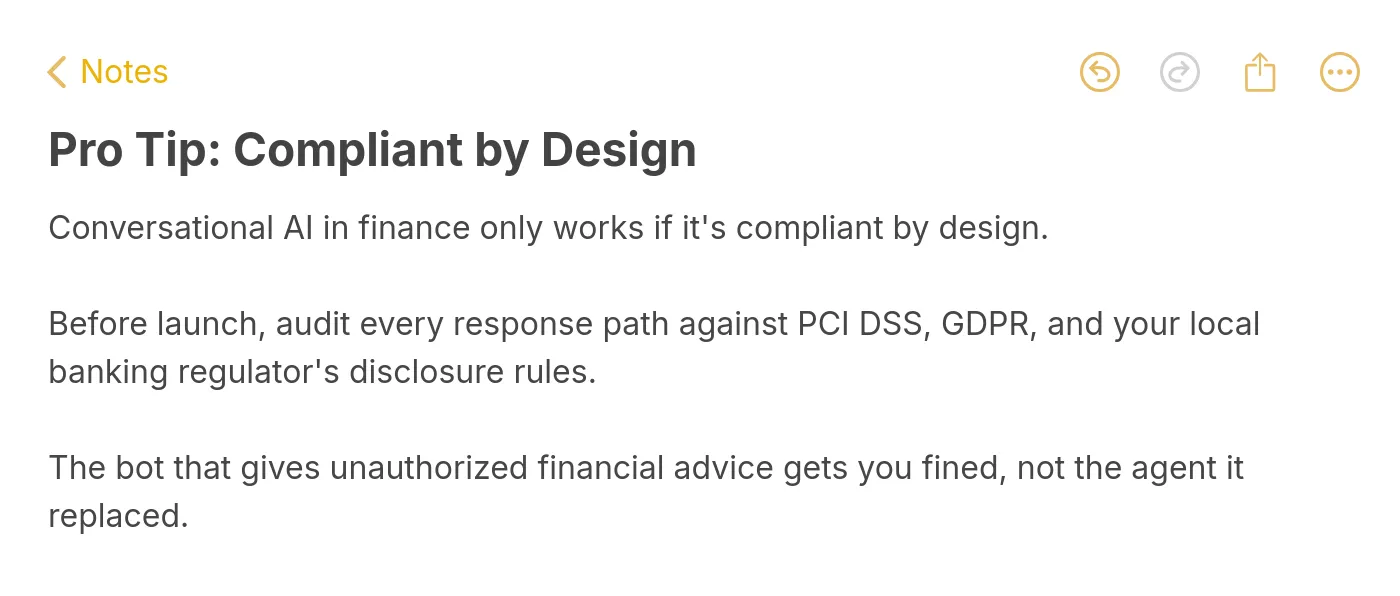

The regulatory environment is the third pressure. PCI DSS 4.0, GDPR enforcement actions, the EU AI Act, and a wave of national banking regulator guidance now expect documented oversight of any AI that talks to customers. Conversational AI platforms built for finance treat that as a feature, with response logging, redaction, and human-in-the-loop review baked in.

Finally, the money is already in motion. According to First Financial Bank, the financial industry is on track to invest nearly $97 billion in AI by 2027, up from $35 billion in 2023, a 29% compound annual growth rate. The teams I see winning are the ones who started a small conversational AI pilot two budget cycles ago and now have the operational data to defend a real line item.

6 high-impact use cases of conversational AI in finance

Across mid-market banks, neobanks, and lending startups, six use cases keep showing up in production. None of them require ripping out the core. They wrap the channels customers already use and the systems agents already work in.

Account inquiries and balance checks

This is the entry-level use case and still the highest-volume one. A customer asks "how much is in my checking" or "did my paycheck land," and the agent authenticates them, calls the core banking API, and answers in plain language.

Personalized financial advice and recommendations

Conversational AI reads transaction history, recurring debits, and cash-flow patterns to suggest the next best action: round-up savings, a higher-yield account, a card-product upgrade, or a debt-consolidation conversation. The bar here is honesty, not cleverness. A good agent will tell a customer they are not eligible for a product instead of pitching it. It also knows when "advice" crosses into regulated investment guidance and steps back to a licensed human.

Loan application and pre-screening

This is where the operational ROI gets obvious. The agent walks an applicant through eligibility questions, pulls income and credit signals through a secure connector, and surfaces a soft pre-approval before a human underwriter ever opens the file. Loan officers stop spending half their day on incomplete applications and only see deals that are actually fundable. Drop-off in the application funnel typically falls 20 to 35% once a conversational agent owns the data-collection stage.

Fraud detection and security alerts

Conversational AI is paired with the bank's fraud engine, not a replacement for it. When a transaction trips a rule, the agent reaches the customer in-channel ("did you just spend $480 in Lisbon?"), confirms or denies, and either clears the transaction or freezes the card and opens a dispute case. Catching fraud in conversation, instead of through a missed phone call, materially shortens the window between detection and containment.

Transaction history and dispute resolution

"What is this charge from JEMSCO LLC" is one of the most common support queries in retail banking, and most of the time the merchant is just a confusing legal name. A conversational agent enriches the transaction with merchant logo, category, and location, and if the customer still wants to dispute, it opens the case, attaches the evidence, and sets expectation on timeline. Agents only see escalations that genuinely need a human.

Compliance and regulatory updates

This use case faces inward as much as outward. Conversational AI can push regulatory updates to internal staff (new fee disclosures, KYC rule changes, updated AML guidance) and answer "is it OK to say this to a customer" questions in real time during a call. On the customer side, it surfaces required disclosures in the natural flow of conversation rather than burying them in a 14-page PDF nobody reads.

Real-world examples of conversational AI in banking

The case studies below are public and well documented. They are useful as a sanity check on what is achievable today, not as a feature wishlist for a vendor demo.

Bank of America's Erica is the most-cited consumer banking deployment in the United States. According to Kayako, Erica handles balance checks, bill reminders, transaction lookups, and goal-based savings nudges directly inside the BofA mobile app, and has surfaced more than a billion customer interactions since launch. The product team's choice to keep Erica narrowly scoped to in-app banking tasks, not open-ended financial advice, is the reason it has held up under regulator scrutiny.

JPMorgan's COiN (Contract Intelligence) is the back-office counterpart. COiN reads commercial loan agreements and extracts the data points that human associates used to spend roughly 360,000 hours a year manually pulling. It is not customer-facing, but it is a clean example of how natural language understanding inside a bank pays off without ever showing up in the app store.

HSBC rolled out an AI-powered virtual assistant across multiple markets to handle retail banking queries in local languages and during local hours. The interesting design decision is the fallback model: when the agent cannot resolve a query, it captures full context and routes the customer (with that context attached) to the next available human agent, so the customer never has to repeat themselves. That single design choice is what makes a conversational AI deployment feel humane instead of hostile.

Capital One's Eno sends proactive alerts about duplicate charges, free-trial conversions, and unusual subscriptions, in addition to handling balance and transaction queries. Eno is also notable for refusing to do things it shouldn't, like share a Social Security number, even when the customer asks. That refusal pattern, often skipped in early deployments, is what an examiner looks for when they ask "show me how the model handles a misuse attempt."

For a wider scan across other industries, our cross-vertical post on chatbot examples covers how the same patterns show up outside finance.

Benefits of conversational AI for financial services

The benefit list below is short on purpose. Vendor decks tend to inflate this section into 12 bullets of overlapping claims. After auditing financial services support flows across mid-market and enterprise teams, these are the six benefits that actually show up in the post-launch numbers.

• 24/7 service without 24/7 staffing: A conversational AI agent answers at 2 a.m. on a holiday with the same accuracy as Tuesday at 11 a.m. Banks recover the customer-experience score they lose when they cap live-agent hours, without hiring a night shift.

• Tier-one cost reduction: Most retail banking inbound is balance, statement, card, and basic dispute questions. Automating that category typically removes 40 to 60% of agent minutes spent on tier-one work, freeing humans for higher-value conversations.

• Scalability during volume spikes: Tax season, fraud incidents, market events, regulator-mandated outreach, all of these create traffic spikes that historically required temporary agents. Conversational AI absorbs the spike at unit cost approaching zero.

• Personalization at population scale: A human relationship manager can know 200 clients well. A conversational agent grounded in the institution's own data can deliver personalized next-best-action across millions of accounts. According to UXDA, about 78% of organizations worldwide already report using some form of AI in at least one business function in 2024, up from 20% in 2017, and personalization is the most common driver.

• Faster fraud response: Reaching a customer in-channel within seconds of a flagged transaction shortens the window between detection and containment, and converts fraud confirmations into a one-tap interaction instead of a missed call.

• Multilingual coverage: Conversational AI handles 40+ languages out of the box, which matters for community banks, credit unions, and international fintechs that historically had to choose which customer segments got native-language support.

Implementing conversational AI in 5 steps

Most failed conversational AI projects in finance fail at the same two stages: data inventory and compliance review. The five-step path below is the one I have seen work, slightly opinionated about where to spend time and where not to.

1. Data and intent inventory: Before you pick a platform, pull six months of support tickets, chat transcripts, IVR logs, and email subjects, and cluster them. You are looking for the top 20 intents that account for 80% of volume. This is unglamorous spreadsheet work and it cannot be skipped. The teams that skip it pick a vendor first and then realize their use case is not what the platform is good at.

2. Model and platform choice: Choose between three architectures: a self-hosted open-weight model, an API-based commercial LLM, or a vertical conversational AI platform. The right answer depends on data residency requirements, internal ML capacity, and budget. For most mid-market banks the platform path wins because compliance and audit features come pre-built, which matters more than raw model quality. If you want a side-by-side perspective from outside finance, our overview of conversational interfaces covers the architecture trade-offs.

3. Compliance and risk review: Run the proposed deployment past your compliance, risk, and InfoSec teams before the first production conversation. Map every response path against PCI DSS, GDPR or local equivalent, AML/KYC obligations, and the EU AI Act if you operate in Europe. Document what the agent will and will not say about products, fees, and investment topics.

4. Pilot with a bounded scope: Pick one channel (in-app chat is usually safest), one customer segment (existing primary-account holders), and one to three intents. Run the pilot for 60 to 90 days with full transcript review by a human QA team. The point of the pilot is not to prove the technology works, it is to find the edge cases your spreadsheet missed.

5. Scale by intent, not by feature: When you expand, expand by adding intents, not by switching channels. A conversational agent that handles 30 intents perfectly on one channel is more valuable than one that handles 5 intents poorly across six channels. Add channels (voice, WhatsApp, web) only after the intent library is mature.

For a related implementation playbook outside finance, our guide on banking AI chatbots covers vendor evaluation criteria in more depth.

Conversational AI in financial services' challenges and risks to manage

Conversational AI in financial services has a different risk profile than e-commerce or hospitality. The cost of a wrong answer is not a refund, it is a regulatory finding. The five risks below show up on every project I've worked on, and each has a concrete mitigation.

Data privacy is the first one. Customer financial data is some of the most regulated data in the world, and any conversational AI deployment has to keep PII inside the institution's perimeter, never leaking it into third-party model training. The mitigation is bring-your-own-model or strict zero-retention contractual terms with whichever LLM vendor you use.

Hallucinations are the second. Generic LLMs will fabricate confident-sounding numbers, and in finance a fabricated APR or fee is a compliance event. The mitigation is grounded retrieval. The model only answers from the institution's verified knowledge base, and any answer it cannot ground gets routed to a human.

Regulatory scrutiny is the third. The EU AI Act, GDPR, the Consumer Financial Protection Bureau in the US, the FCA in the UK, and a growing list of national regulators are publishing specific guidance on AI in customer-facing financial services. The mitigation is treating compliance as an architecture decision, not a launch-week checkbox, and keeping a documented audit trail of every customer-facing response.

Customer trust is the fourth, and the easiest to underestimate. Customers will tolerate a bot that says "let me get a human for this" and they will not tolerate a bot that pretends to be human and gets caught. The mitigation is transparent disclosure on first turn, every turn.

Integration complexity is the fifth. Core banking systems are old, queues are batched, and APIs are uneven. Most conversational AI projects underestimate the integration work by 2 to 3x. Budget for it, scope the pilot to the systems that already have clean APIs, and tackle the rest in phase two.

Pilot a Conversational AI Use Case This Quarter

Don't try to automate everything at once. Pick one intent, balance inquiries, fraud confirmations, or loan pre-screening, run a 60 to 90 day pilot inside the channel your customers already use, and measure containment, CSAT, and compliance audit results against your current human-only baseline. The teams that win with conversational AI in financial services are the ones who shipped a small thing in 2025 and now have the operational data to defend a real budget line in 2026.

Frequently asked questions

How does conversational AI improve personalized financial advice?

Conversational AI reads a customer's transaction history, spending patterns, savings rate, and stated goals, and uses that to suggest the next best action: a higher-yield account, a debt-consolidation conversation, a card upgrade, or a savings nudge. It does not replace a licensed financial advisor for regulated investment guidance, but it covers the day-to-day "what should I do next with my money" questions that customers used to never get answered at all.

What role does conversational AI play in loan processing?

It owns the front of the funnel. The agent walks an applicant through eligibility questions, pulls income and credit signals through a secure connector, identifies missing documents, and surfaces a soft pre-approval before a human underwriter touches the file. Loan officers stop spending half their day on incomplete applications, and applicants get a faster yes-or-no answer instead of waiting three days for a callback.

How can conversational AI enhance compliance and regulatory adherence in financial services?

It logs every customer interaction in the same case-management system the compliance team already audits, surfaces required disclosures inside the natural flow of conversation, and pushes regulatory updates to internal staff in real time. The agent itself is bounded by what regulators allow it to say, with hard guardrails on regulated topics like investment advice, insurance recommendations, and credit terms.

How long does it take to deploy a conversational AI agent in a bank?

A bounded pilot, one channel, one segment, three intents, typically takes 8 to 12 weeks from kickoff to first production conversation. Scaling from a pilot to a full intent library covering 70 to 80% of inbound volume takes another 6 to 9 months. Banks that try to do it all in one push usually spend 18 months and ship nothing.

Is conversational AI in finance the same as a chatbot?

No. A chatbot follows a scripted decision tree and breaks the moment a customer phrases a question differently. Conversational AI uses NLP to handle paraphrased questions, holds context across turns, calls APIs to take action (move money, freeze a card, open a dispute), and hands off to a human with full context attached. The user-visible difference is whether the experience feels like a phone tree or a conversation.

For further reading, you might be interested in the following:

Banking AI Chatbots: How to Use, Benefits, Use Cases