The best banking chatbots for 2026 are LiveChatAI, ChatBot, Kore.ai, Jasper AI Chat, Intercom Fin, and Sendbird. We evaluated each on data security, regulatory posture, integration depth, training flexibility, language coverage, and pricing transparency so banking teams can shortlist the right fit and pilot one this quarter without rip-and-replace risk.

What is a banking chatbot?

A banking chatbot is an AI assistant that handles customer-facing or internal banking tasks through chat or voice — checking balances, moving money, triaging fraud alerts, qualifying loans, answering policy questions, and routing complex cases to a human banker with the right context attached.

The scope matters because banking is not generic customer service. A chatbot that helps a retailer track a parcel can be wrong and the customer shrugs. A chatbot that misreads a wire instruction, mishandles a dispute, or leaks an account number creates a compliance incident. So the technology layer is similar to other AI bots, but the guardrails are not — banking chatbots have to authenticate users, log every exchange, respect PCI-DSS and GLBA boundaries, and hand off cleanly the moment a question stops being routine.

I'm Perihan from LiveChatAI, and across the financial-services accounts I work with, the pattern is consistent: the teams that succeed treat the chatbot as a first-line agent, not a magic deflector. They scope it tightly to authenticated balance inquiries, FAQ deflection, card services, branch and ATM lookup, and pre-qualification flows — and they leave fraud-decisioning and dispute resolution to humans with the bot doing intake. That separation of duties is what makes the deployment safe enough to ship.

If you want a wider read on how this overlaps with insurance, wealth, and fintech use cases, our piece on conversational AI in finance walks through six concrete patterns we see across the sector.

Why banking chatbots matter in 2026

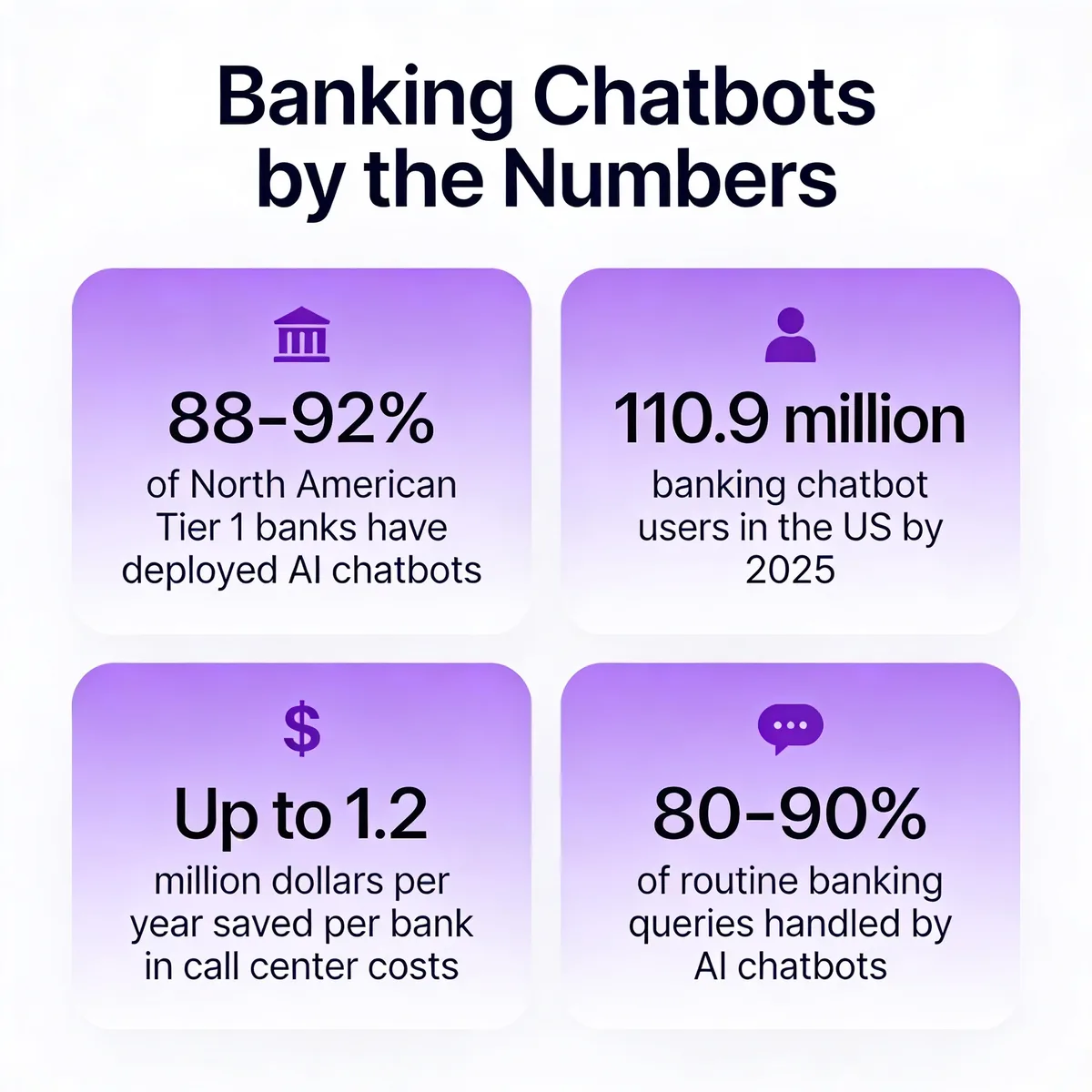

Banking has crossed the line from "experimenting with chatbots" to "running on them." According to Azumo's 2025 banking AI report, 88-92% of North American Tier 1 banks have integrated AI chatbots, and every one of the top 10 commercial banks now runs at least one production bot. The same data set puts US banking chatbot users at 110.9 million by 2025, which is roughly one in three American adults already talking to a bank bot.

The savings line up with the adoption. According to Master of Code's banking-chatbot benchmark, AI-powered banking bots cut call-center costs by up to $1.2M per year per institution and handle 80-90% of routine queries — the kind of volume that used to require a 40-seat overflow team during tax season. Juniper's earlier framing, that chatbots save the sector around $8 billion annually and shave more than four minutes off the average enquiry, still tracks with what we measure inside customer deployments.

The market is still climbing. According to a LinkedIn industry brief on chatbot-based banking, the segment was valued at $3.2B in 2024 and is on track for $9.5B by 2033 — and adoption outside North America is moving faster than people expect. SQ Magazine's regional breakdown puts Southeast Asia at roughly 73% adoption in 2025, ahead of several mature markets.

What's changing for 2026 is the shift from "answer questions" to "complete tasks." Gartner, cited in a 2026 banking chatbot roundup from Zowie, projects agentic AI will resolve 80% of common customer-service issues by 2029 with a 30% cost reduction. Inside banking, that translates to bots that can file a dispute, freeze a card, schedule a wire approval, and pull statements — not just narrate where to click.

Key elements of an effective banking chatbot

The difference between a banking bot that ships and one that gets quietly pulled in month three is almost never the LLM. It's whether these seven elements were designed in from day one.

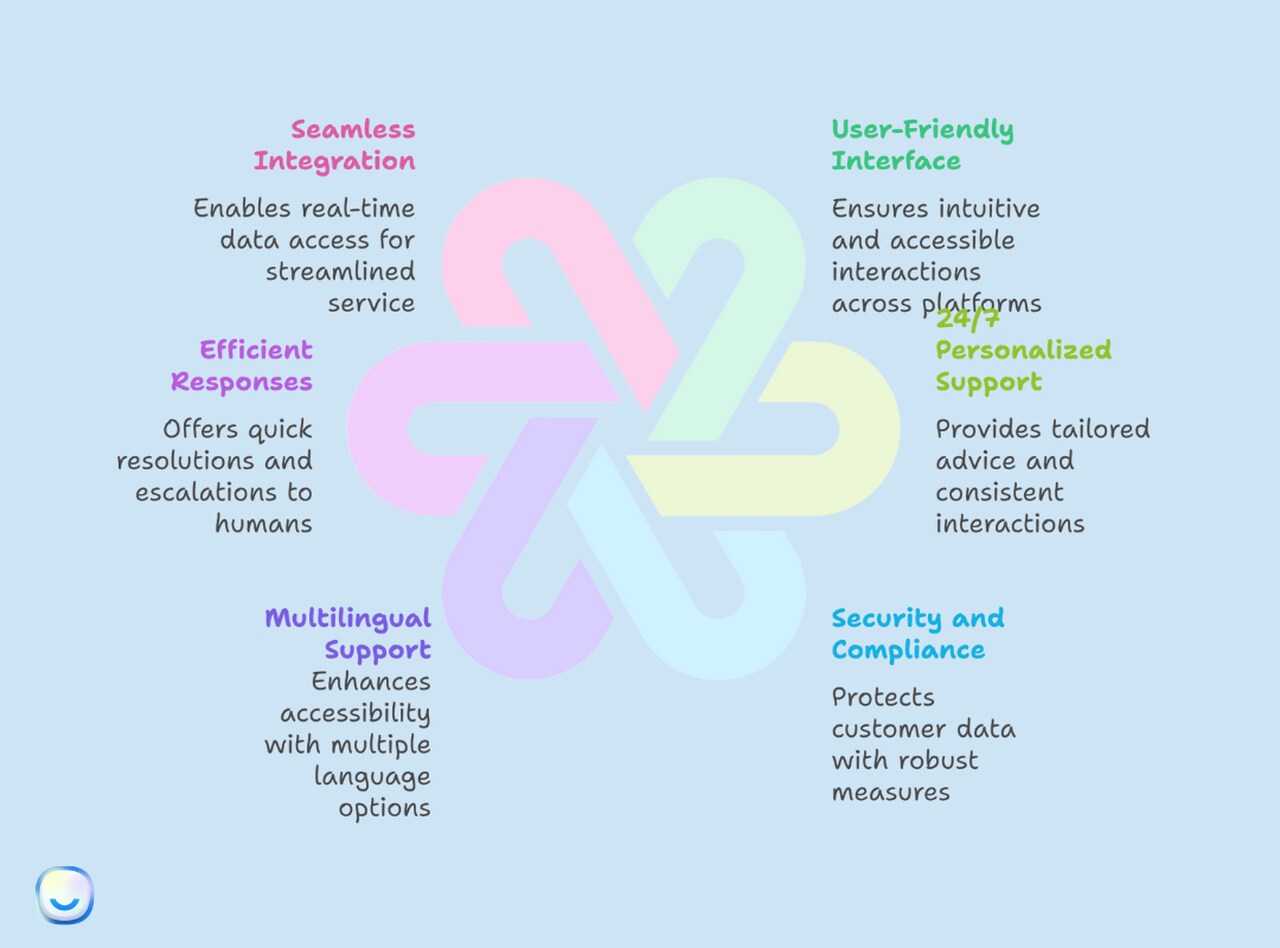

End-to-end data security: Encryption in transit and at rest is table stakes. What I look for in financial deployments is data minimisation — the bot reads only the fields it needs (last 4 of card, masked account ID, transaction ref) and never logs the full PAN. Vendor SOC 2 Type II and ISO 27001 reports should be available without a sales call.

Regulatory compliance posture: PCI-DSS for card data, GLBA and the FFIEC chatbot guidance in the US, GDPR for any EU customer, and the CFPB's 2023 chatbot-in-consumer-finance report all set the floor. Ask the vendor for a written compliance matrix mapped to your specific regulators — if they hand-wave it, that's the answer.

Authentication and step-up auth: A banking bot should know the difference between "what's my routing number" (public) and "transfer $4,000 to a new payee" (high-risk). Step-up flows — biometric, OTP, in-app confirmation — should be configurable per intent, not bolted onto every interaction.

Multi-channel parity: Customers expect the same answer on web, mobile app, WhatsApp, voice, and sometimes Apple/Google Business Messages. Channel parity isn't a nice-to-have. It's how you stop the "I asked the bot on Wednesday and got a different answer Friday" complaint that kills trust.

Clean human handoff: The bot has to know when to stop. A good handoff carries the entire conversation transcript, the customer's identity context, and the detected intent into the agent's queue — not "Chatbot transfer, no context." We see CSAT swings of 15 points on this single element.

Audit logging and explainability: Every response, source citation, and action the bot takes has to be reconstructable for a regulator, an internal auditor, or a customer dispute. If the vendor can't show you the audit trail UI in a demo, the bot can't live in a regulated environment.

Graceful fallback: When the bot doesn't know, it says so and offers a path. "I'm not sure — would you like me to connect you to a banker?" beats hallucinating a fee schedule every time. Confidence thresholds should be tunable per intent so high-risk intents fail safe.

Benefits of banking chatbots for financial services

I've watched mid-sized credit unions and tier-2 commercial banks deploy bots over the last three years, and the benefits cluster into a predictable set. None of them require a moonshot to capture.

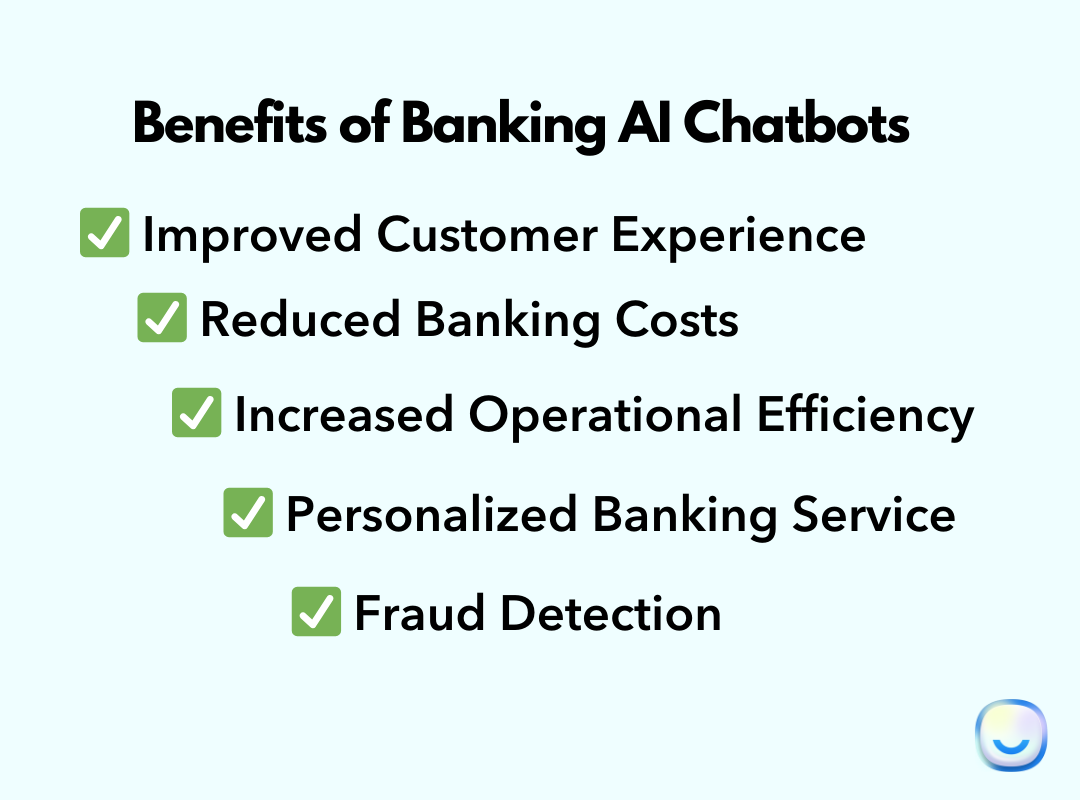

24/7 availability without staffing penalty: The 11pm balance check, the Saturday card freeze, the Sunday-night statement request — these are the volume drivers that used to push call centres to 24/7 staffing they couldn't justify. A bot covers the overnight tail at zero marginal cost per interaction.

Routine query deflection: Balance inquiries, recent transactions, branch hours, ATM locations, routing numbers, statement copies, and password resets together account for the bulk of contact volume at most retail banks. A focused bot resolves 60-80% of that traffic before a human ever touches it.

Measurable cost reduction: Beyond the headline $1.2M figure, the savings show up in average-handle-time on the calls that do escalate — humans spend less time on look-ups because the bot has already pulled the account context and surfaced the likely answers.

Fraud detection assist: According to Gitnux's 2023 banking AI dataset, 76% of banking executives reported they had implemented AI-driven fraud detection systems — a 15-point jump year over year. Chatbots feed that pipeline by triaging suspicious-transaction alerts conversationally and capturing customer responses in seconds instead of waiting for a callback.

Lead qualification for lending and onboarding: A bot that pre-qualifies a small-business loan applicant — collecting time-in-business, revenue, intended use of funds, and credit-score range — hands a hot lead to a banker in five minutes instead of forty.

Customer self-service that customers actually like: When the bot is fast and accurate, customers prefer it to phone. They don't want to talk to a human about why their statement isn't downloading — they want the statement.

Language inclusivity: Multilingual banking is hard with humans because you need bilingual staff in every shift. A multilingual bot covers 40-80 languages from day one, which matters for credit unions serving immigrant communities and for international banks with cross-border customers. Our deeper read on omnichannel chatbots covers how language and channel intersect.

Best practices for deploying banking chatbots

If I could give one piece of advice to a banking team about to kick off a chatbot project, it would be this: pick the boundary of the deployment before you pick the vendor. The teams that struggle are the ones that buy a platform first and then argue for nine months about what it should do.

Data privacy by design: Decide what data the bot can read and what it cannot, in writing, before procurement. Run a DPIA. Treat the chat log itself as PII. If the vendor stores transcripts on infrastructure you can't audit, that's a deal-breaker, not a footnote.

Persona-based testing before launch: Build a test plan around five to seven customer personas — the elderly customer asking about a fraud alert, the small-business owner trying to add a payee, the international student opening their first account, the customer trying to dispute a duplicate charge. The bot should pass every persona's top three intents before it sees a real customer.

Compliance-first prompt design: Every system prompt should include the regulatory boundary — "do not provide investment advice," "do not promise approval for any product," "do not quote interest rates that aren't pulled from the live rate API." Hard-code refusal language for out-of-bounds requests.

Escalation paths mapped per intent: Not every miss escalates to the same queue. Fraud goes to fraud. Wire holds go to ops. Account opening goes to onboarding. Map it once, codify it in the bot, and stop the universal "transfer to agent" routing that floods one team.

Multilingual support that's tested, not just enabled: Switching the language toggle on isn't multilingual support. Run native-speaker QA on every priority intent in every supported language. Banking terminology mistranslates badly — "overdraft" alone has three or four distinct equivalents across Spanish-speaking markets.

Transparency about AI: Tell the customer they're talking to a bot. The CFPB has been explicit about this, and customers handle it fine when the bot is competent. The trust hit comes from pretending to be human and failing, not from being a bot.

Tightly scoped knowledge base: Train on your own product docs, policy PDFs, FAQ pages, and tariff schedules. Do not let the bot answer from the wider internet on regulated topics. Scoping is what separates "useful" from "litigable."

The 6 best banking chatbots for 2026

We evaluated each vendor below on data security, regulatory posture, integration depth, ease of training on your own data, language coverage, and pricing transparency. I've worked hands-on with LiveChatAI for years and have evaluated the others through demos, customer-reported migrations, public documentation, and the kind of side-by-side bake-offs banking teams run before procurement. Where pricing is not publicly disclosed, I've said so rather than fabricate a number.

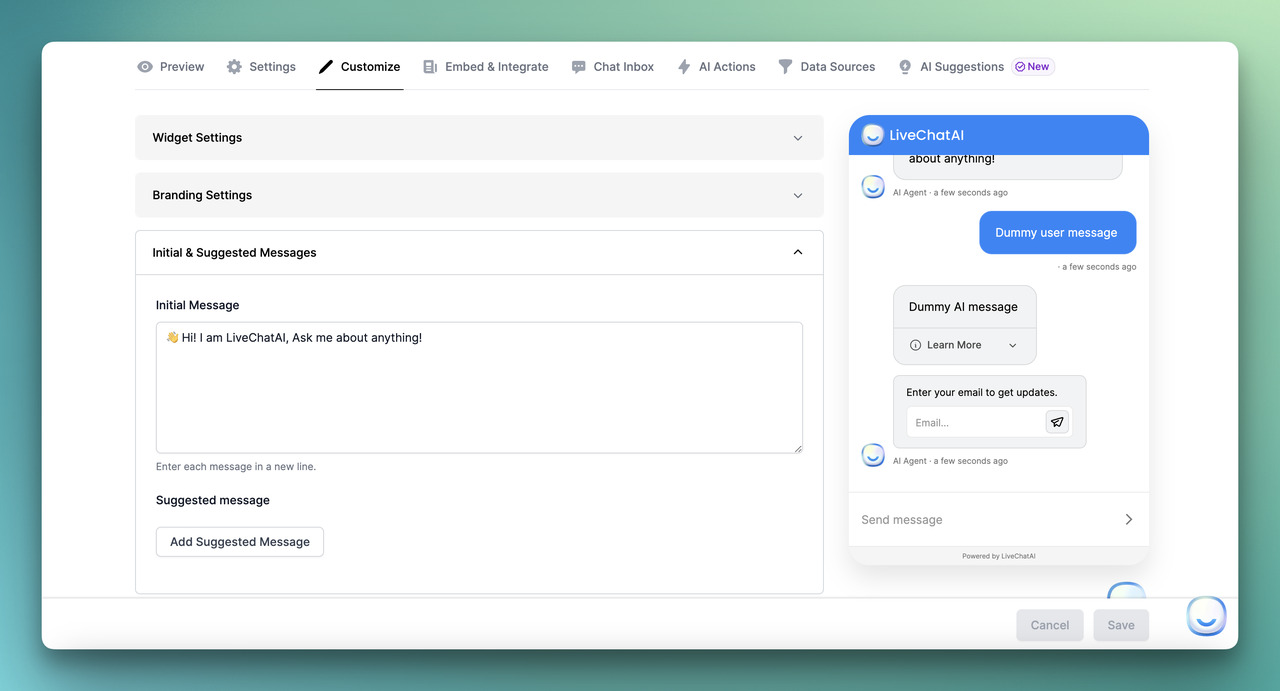

1. LiveChatAI

Best for: Mid-sized banks, credit unions, neobanks, and fintechs that want a chatbot trained on their own help docs, policies, and product pages in days rather than months — and want to keep the door open to a human agent the moment the conversation gets complex.

LiveChatAI is our platform, so I'll be direct about where it fits and where it doesn't. It's a customer-data-trained AI chatbot that ingests websites, sitemaps, PDFs, Q&A pairs, and help-centre exports, then answers questions from that scoped knowledge base using the LLM of your choice (GPT-4 class, Claude, or open-source). For banking, that scoping is the point — the bot doesn't go fishing on the open web for an answer to "what's your overdraft policy."

Why it fits banking: Three things matter when a bank evaluates a platform — data control, integration into existing CX stacks, and the ability to escalate to a human banker cleanly. LiveChatAI lets you train on documents you control, embed the bot on your site, app, WhatsApp, Slack, or via API, and hand off to a live human in the same widget. Conversation transcripts are exportable for audit, and prompt-level controls let compliance teams cap what the bot is allowed to say.

Integration depth: Native integrations with Make, Zapier, Webhooks, and OpenAPI mean you can wire the bot into Salesforce Financial Services Cloud, Mambu, FIS, or whatever core banking system you run. We have customers piping conversation events into Snowflake and Looker for retention analysis.

Training and customisation: You point it at your knowledge sources, set the tone, set the response temperature, and ship. In our testing across banking customers, the median time from account creation to a production-ready bot answering the top 20 retail intents is under two weeks — most of that is the bank's QA cycle, not the platform.

Security posture: SOC 2 Type II, GDPR-aligned data handling, configurable data residency, and conversation-level deletion. We never train shared models on customer data — each customer's knowledge base is isolated.

Pricing: Public, tiered, and predictable — free trial available, paid plans scale by message volume and team seats. Enterprise contracts include data residency choice, SSO, and a dedicated success contact. You can do the math on a payback period yourself with our chatbot ROI calculator.

Honest cons: If you need a full IVR-style voice deployment with sub-200ms latency on the phone, this isn't the right tool — we focus on chat and async channels. And if your bank requires on-prem-only deployment because of national data laws, you'll want to talk to us about deployment options early.

Example use case: A regional bank we worked with deployed LiveChatAI as the first-line for their help centre. Within six weeks, the bot was deflecting roughly 65% of inbound chat tickets and handing the rest to live agents with the full conversation context. Average resolution time on escalated tickets dropped because agents stopped re-asking the same identifying questions. For more banking-flavoured patterns, see our chatbot use cases guide.

2. ChatBot

Best for: Banks and credit unions that want a visual, flow-based bot builder with templates and predictable behaviour, and that don't need a generative LLM doing free-form Q&A on regulated topics.

ChatBot is a flow-builder-first platform. You design conversation paths using a drag-and-drop canvas, mix in some NLP for intent matching, and ship. That makes it a natural fit for banks that want every customer journey explicitly designed and approved — the system prompt isn't open-ended because there isn't really a system prompt in the LLM sense.

Why banks consider it: Compliance teams find it easy to defend. Every path is mapped, every response is pre-authored, and there's no model temperature to worry about. For a bank that has been burned by generative hallucinations or whose regulator is sceptical of probabilistic answers, that determinism is worth a lot.

Integration depth: Web, mobile, Facebook Messenger, Slack, LiveChat, and a REST API. Solid for most retail-banking footprints, though you'll want to confirm support for any specific CRM or core banking system in a demo.

Training and customisation: "Training" here means designing flows and seeding intent-matching examples. There's no upload-your-docs-and-go shortcut. For a bank with a tightly defined set of top 30 intents, that's fine. For a bank that wants the bot to answer anything in its 4,000-page knowledge base, this isn't the model — and that's a feature, not a bug, depending on your risk appetite.

Security posture: GDPR alignment, role-based access, and conversation logging. Validate SOC 2 status and data-residency options directly in procurement.

Pricing: Tiered by chat volume and team size, published on their site. The mid-tier is comfortable for a single-bank-brand deployment; enterprise tiers cover multi-brand portfolios.

Honest cons: The flow-builder model means every new intent is a new design ticket. As your bot's surface area grows past ~75 intents, maintenance gets non-trivial. Also, there's no on-the-fly long-tail Q&A — if a customer phrases something outside the trained intent set, the bot falls back. For some banks that's exactly the safety they want; for others it's a coverage gap.

Example fit: A small community bank with 25-40 well-defined customer intents and a compliance team that wants every word the bot says signed off by legal. ChatBot is a defensible, mature pick for that use case.

3. Kore.ai

Best for: Large enterprise banks running a full omnichannel virtual-assistant programme across voice, chat, mobile, and web — with budget for a long implementation cycle and an internal team to maintain it.

Kore.ai is one of the more banking-specialised players in the comparison set. Their BankAssist offering is a pre-packaged virtual assistant trained on 250+ retail-banking use cases out of the box — balance inquiries, fund transfers, bill pay, card services, account opening, and the rest of the retail-banking long tail. They've sold heavily into tier-1 commercial banks and are a frequent shortlist name when the deal value runs into seven figures.

Why banks consider it: The 250+ pre-trained intents are a real shortcut. You're not starting from scratch on conversation design. The platform also covers voice (IVR-grade), chat, mobile, and web with the same intent layer, which is a fit for banks that want one orchestration brain across every channel.

Integration depth: Strong. Connectors to Salesforce, ServiceNow, core banking platforms, and a sophisticated dialogue management layer. Voice deployment with telephony providers is a first-class capability, not an afterthought.

Training and customisation: The flip side of "250 use cases out of the box" is that customising them to your specific products, fees, and policies is a multi-month consulting engagement, often with Kore.ai's professional services or a partner SI. Plan for it.

Security posture: Enterprise-grade certifications, on-prem and private-cloud deployment options. This is where Kore.ai wins versus pure-SaaS competitors in markets with strict data-residency rules.

Pricing: Not publicly listed. Expect enterprise contracts with implementation fees on top of platform licensing. Budget six figures minimum for a full retail-banking deployment.

Honest cons: The same things that make it strong for tier-1 — depth, configurability, on-prem options — make it heavy for tier-3 banks and credit unions. The implementation timeline is measured in quarters, not weeks. If you're a regional bank with a small product team, Kore.ai is probably the wrong tool. If you want lighter alternatives mapped against it, we keep an updated piece on Kore.ai alternatives.

Example fit: A top-50 commercial bank rolling out a unified virtual-assistant programme across phone, web, and mobile, with the team and budget to support a 9-18 month rollout.

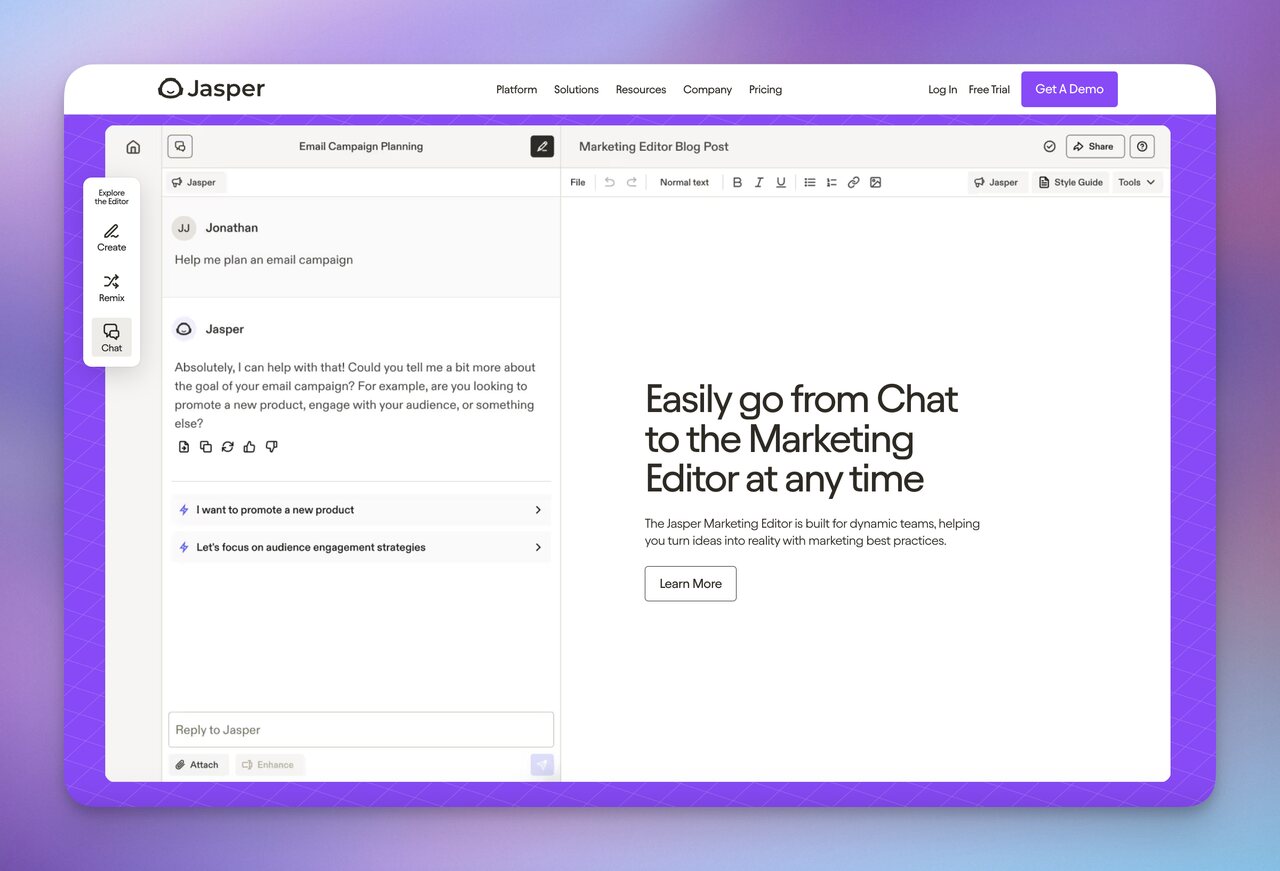

4. Jasper AI Chat

Best for: Bank marketing teams that want a chat-style interface for drafting customer comms, blog posts, social copy, and campaign briefs. Not for customer-facing banking conversations.

I want to be transparent here, because Jasper AI Chat shows up in roundups like this and the reality is it's mostly a content-creation tool with a chat UI. It's excellent at writing marketing copy, paraphrasing long-form content, drafting newsletter sections, and helping a marketing team move faster. It's not a customer-service bot, and it doesn't pretend to be one.

Why it shows up on banking lists at all: Marketing teams inside banks use it the same way marketing teams everywhere use it — to scale content output. If a bank's content team is producing twice-weekly blog posts about financial literacy, mortgage explainers, and product launches, Jasper makes that workload manageable. That's a legitimate use case. It's just not the same as fielding customer questions.

Integration depth: Browser extensions, integrations with the major content platforms (Google Docs, WordPress, the social schedulers), and an API. None of that is geared at core-banking integration because that's not the product's intent.

Training and customisation: Brand voice templates and a "Knowledge Base" feature for keeping brand facts consistent. Useful for marketing voice. Not designed for ingesting your account-policy PDFs and serving them to customers in chat.

Security posture: Standard SaaS security for a marketing tool. Don't put customer PII into it. Don't paste account numbers. Use it for marketing copy and stop there.

Pricing: Per-seat SaaS, public on the site. Reasonable for a marketing team of five to fifty.

Honest cons: If you came to this list looking for a chatbot to put in front of banking customers, Jasper AI Chat is the wrong tool. It's a writing assistant. Buy it for the marketing department, not the contact centre. We've covered the broader category of writer-assistants and conversational tools in our piece on conversational AI examples if you want to see where each lives.

Example fit: A bank's content marketing team that wants to ship more financial-education content faster, with brand-voice consistency, and is comfortable having a human editor in the loop on everything that ships.

5. Intercom Fin

Best for: B2B-leaning fintechs and digital-bank operations teams already on Intercom, who want a generative AI agent on top of their existing help-centre and inbox.

Intercom's Fin is a generative AI agent that sits on top of Intercom's existing messaging, inbox, and help-centre. It uses your support content — articles, macros, internal docs — as its knowledge source and answers customer questions with citations back to the source article. For shops already standardised on Intercom as their CX platform, it's almost a flip-of-a-switch deployment.

Why fintechs consider it: If your support team already lives in Intercom — using their inbox, ticketing, and help centre — adding Fin is a much smaller change than ripping in a separate bot platform. The handoff to a human agent happens in the same UI, the same workflows, the same SLAs.

Integration depth: Native to the Intercom platform. Connectors to Salesforce, HubSpot, Slack, and a public API. Less native into core banking platforms than Kore.ai or LiveChatAI, but for digital-only banks and fintechs that's usually not the gating constraint.

Training and customisation: Fin reads your Intercom help-centre articles and any uploaded content. You set the persona, tone, escalation rules, and confidence thresholds. Language coverage extends to 45+ languages, which is plenty for most fintech audiences.

Security posture: SOC 2, GDPR, HIPAA available on higher tiers. Validate the specific compliance package against your jurisdiction in procurement.

Pricing: Per-resolution pricing in addition to Intercom seat costs. The per-resolution model can be very efficient at high volume, but it also means you need to forecast resolution counts carefully or the bill surprises you. Get a sample invoice from a similar-volume customer before signing.

Honest cons: Tightly coupled to Intercom — if you're not on the platform already, the total cost of adoption is much higher than Fin's licence alone. The per-resolution pricing model needs careful modelling. And for retail banks with deep core-system integration needs, the Intercom ecosystem is less mature than Kore.ai or a dedicated platform.

Example fit: A digital-only neobank or fintech with 50-500 support staff already running on Intercom, looking to deflect 40-60% of their inbound chat volume to AI without changing their workflow.

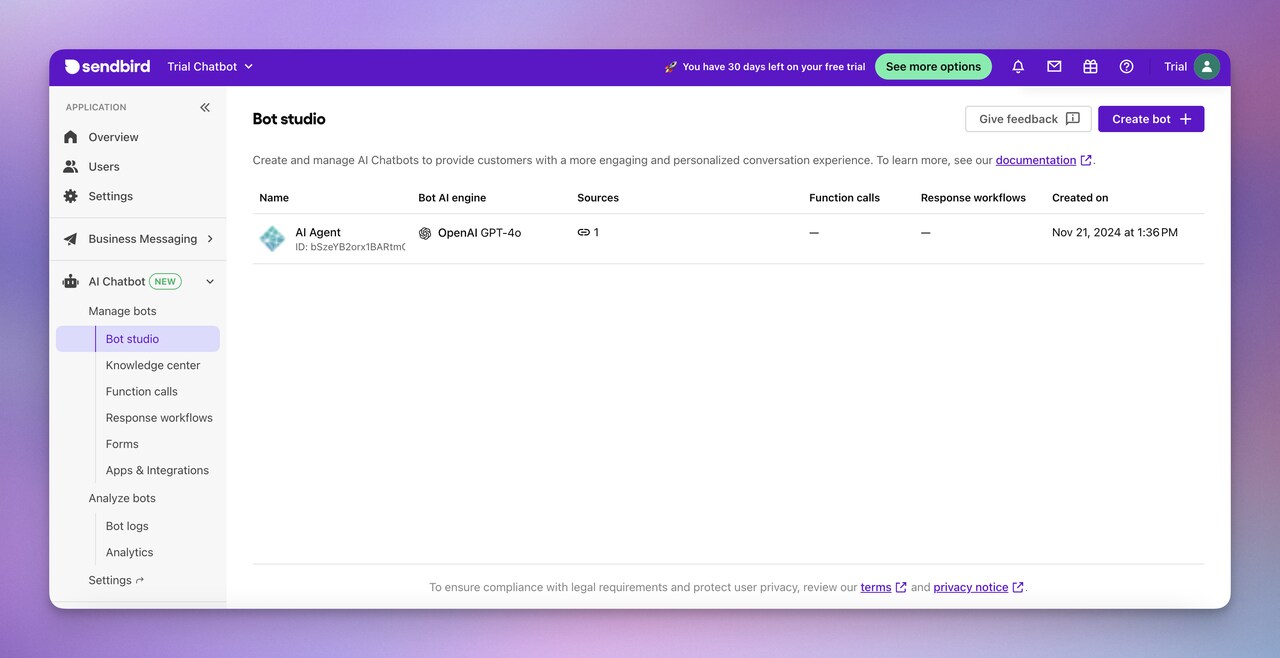

6. Sendbird

Best for: In-app messaging-first banks and fintechs that want chat, voice, and AI agent all wrapped into one SDK inside their mobile app — and who care more about messaging primitives than CX-suite features.

Sendbird started as a messaging SDK — chat, voice, video — embedded in mobile apps. They've layered AI agents on top, and the resulting product is a fit for banks that already use Sendbird (or a similar messaging SDK) inside their mobile banking app and want to add AI conversation as another channel inside that same surface.

Why fintechs consider it: The SDK-first approach means everything lives natively inside your app. No iframe, no third-party widget, no separate domain. For mobile-first banks where the app is the primary customer surface, that level of integration matters for both UX and security perimeter.

Integration depth: Strong on the messaging side — chat, voice, video, push, threaded conversations. Less geared at integrating with traditional contact-centre stacks (Genesys, NICE) than Kore.ai, but stronger as a mobile-app SDK than most competitors here.

Training and customisation: AI agent layer reads your knowledge base content; over 80 languages out of the box. Configurable handoff to human agents and analytics on conversation quality.

Security posture: GDPR and SOC 2 compliant. Visual verification capabilities. Validate against your specific jurisdictional rules before signing.

Pricing: Mixed — message volume, monthly active users, and per-feature add-ons. The model rewards efficient design and penalises sprawling deployments. Model your usage before you commit.

Honest cons: If your customer experience lives on the web more than the mobile app, Sendbird's mobile-first DNA leaves you using only half the product. And the integration with non-Sendbird CX tools (Salesforce, Zendesk) is less mature than competitors that started in those ecosystems.

Example fit: A mobile-first neobank or fintech with 100k+ MAU on the app, wanting to add an AI agent inside the existing in-app chat without bolting on a new vendor surface.

How to choose the right banking chatbot for your team

Six vendors is too many to evaluate seriously. The shortlist usually narrows to two or three once you've answered the questions below. Skip ahead to whichever cluster applies and the rest of the noise drops away.

Scope: customer-facing or internal? A customer-facing retail-banking bot has a very different risk surface from a bot that helps relationship managers look up account data. If the project is internal-only, you can pick lighter-weight tools and prioritise speed over compliance breadth. Customer-facing means the full compliance matrix is non-negotiable.

Compliance requirements: Which regulators sit in scope — OCC, CFPB, FDIC, FCA, MAS, BSP? Get a written compliance map from each shortlisted vendor before the demo. If the vendor pushes back on putting it in writing, that's the signal.

Deployment model: Cloud-only is fine for most digital banks. Tier-1s and any bank in jurisdictions with strict data-residency laws need private-cloud or on-prem options. That requirement alone cuts the shortlist in half.

Integration depth: Inventory the systems the bot has to read from and write to — Salesforce Financial Services Cloud, Mambu, FIS, Temenos, your fraud-platform, your IVR, your help-centre CMS. Score each vendor on native connectors versus "you can build it with our API." The difference between native and API is six months of integration work.

Training data model: Do you want a bot trained on your own docs (LiveChatAI, Intercom Fin), one with pre-trained banking intents you customise (Kore.ai), or one with manually designed flows (ChatBot)? There's no single right answer — but pick consciously, because the maintenance model differs.

Pricing model: Seat-based, message-based, resolution-based, or per-MAU? Each model rewards different deployment shapes. Match the pricing model to your expected usage curve, not just the headline price.

Support and success quality: A banking deployment is not a self-serve project. Ask each vendor for two reference customers in banking. If they can't produce two, that tells you what their banking traction actually is.

How to build a banking chatbot with LiveChatAI

Here's the short version of what a banking team does in week one with LiveChatAI. None of this requires engineering effort beyond pasting a snippet into your site or app.

Step 1: Create a LiveChatAI account

Create a LiveChatAI account and create your first AI bot. The free tier lets you build and test before you commit a budget.

Step 2: Pick your training data sources

Most banking teams start with the public website and the help-centre. The platform crawls a website or sitemap, ingests uploaded PDFs (policy docs, fee schedules, product brochures), and lets you paste Q&A pairs manually. For a regulated environment, only feed it documents that are already approved customer-facing — don't upload internal-only docs.

Step 3: Tune the bot persona and prompts

Set the name, persona, tone, system prompt (with explicit refusals for out-of-scope topics), response temperature, and fallback message. For banking, I push customers to a low temperature (more deterministic) and a clear "I'm not sure — let me connect you to a banker" fallback.

Step 4: Configure escalation rules

Decide which intents always escalate to a human (disputes, fraud, wire holds), which intents the bot can fully resolve (balance, branch hours, statement requests), and which intents the bot resolves with a human-confirm step (payee additions, profile changes).

Step 5: Run persona-based testing with compliance sign-off

Spin up five to seven test conversations covering the priority customer journeys. Have a compliance reviewer sign off on the bot's actual responses, not just the design doc.

Step 6: Embed the bot and monitor week one closely

Paste the embed snippet into your site, app, or WhatsApp Business workflow. Monitor the first two weeks closely — fix any falsely-confident answers immediately and tighten the system prompt as you find edge cases. Browse our broader library of chatbot examples for design inspiration during this phase.

Use cases for AI chatbots in banking

The use cases below are the ones we see banks actually ship — not theoretical possibilities. Each one maps to measurable contact-centre volume and can be deployed independently.

Account inquiry and balance checks

The single highest-volume intent at most retail banks. Authenticated balance lookup, recent transaction list, scheduled-payment review. Bots handle it in seconds, 24/7, with no agent in the loop.

Fraud alert triage

Customer gets a suspicious-transaction alert, replies in chat, bot confirms or denies the transaction, escalates to fraud ops only if the customer disputes. Cuts fraud-team workload on legitimate transactions to near zero.

Loan and credit pre-qualification

Bot collects time-in-business, revenue, requested amount, intended use, soft credit pull preference. Hands a qualified lead to a banker with the entire intake already complete. Cycle time from inbound to banker callback drops from days to hours.

Card services and dispute intake

Lost-card freezing, replacement-card ordering, travel-notice posting, PIN reset initiation, dispute filing intake. All of it routine, all of it deflectable. The bot captures the disputed transaction details, the customer's narrative, and supporting evidence, then creates the case in the dispute platform — saves both sides 10-15 minutes per dispute.

Branch and ATM finder

Geolocation-aware search inside the conversation. Far better experience than "go to our website and click 'find a branch.'"

Transaction history and statement requests

Pull the last 90 days of activity, generate and email a statement, schedule a recurring monthly delivery. All without a human.

Financial education and product guidance

Bot explains overdraft fees in plain language, walks through the difference between savings products, answers "what does APR mean" without lecturing. Customers ask financial-education questions constantly and they're a perfect bot intent.

Regulatory help and disclosures

Sourcing the right disclosure language, walking customers through Reg E protections, pointing to the right form for a complaint. The bot's job is to surface the right link and the right plain-English summary — not to interpret regulation.

Shortlist three banking chatbots and pilot one this quarter

If you take one thing from this evaluation, take this: the cost of waiting another year is higher than the cost of picking imperfectly and iterating. The data is clear — 88-92% of Tier 1 banks already run a chatbot, the routine-query deflection is real, and the agentic-AI wave Gartner has been forecasting is going to make today's bots look static by 2027. Pick two or three vendors from the six above that match your scope and your compliance posture. Demo each against the same three customer personas. Pilot the winner in one narrow use case — card services, or balance inquiries, or fraud-alert triage — and measure deflection and CSAT for six weeks. Then expand. Whatever you do, don't run another nine-month vendor selection on a project that should be live by end of quarter. For more on what the chatbot space looks like outside banking, our library of chatbot business ideas is a useful adjacent read.

Frequently asked questions

What impact do AI chatbots have on customer engagement in mobile banking apps?

Inside the mobile banking app, AI chatbots increase engagement because they remove friction at the moment of intent. A customer who would have given up trying to find "how to add a payee" in a four-tap menu just asks the bot. We see app session length and feature adoption both rise after a bot launch — proactive nudges (bill-pay reminders, statement-ready notifications, low-balance alerts) inside the same chat surface drive 15-25% more interactions per active user in the first three months.

How can AI chatbots support regulatory compliance in banking?

Chatbots help compliance teams in three concrete ways. First, every conversation is logged and timestamped, so audit trail for regulators is automatic instead of patched together from phone notes. Second, the bot can enforce hard refusals for out-of-bounds topics — "do not provide investment advice," "do not quote interest rates without pulling from the live rate API" — at the system-prompt layer, which means compliance is encoded once and enforced every conversation. Third, disclosure delivery is consistent — the bot sends the same Reg E summary, the same Truth-in-Lending language, every time, with no human variability.

Can AI chatbots be used to improve internal banking operations?

Yes, and this is often the easier first deployment because the regulatory burden is lower. An internal bot for relationship managers can pull account context, summarise customer history, search policy docs ("what's our wire cutoff for international USD?"), and draft response emails. A bot for onboarding new branch staff can answer "how do I process a deceased-customer account closure" without pulling a senior banker off the floor. Internal bots are typically live in three to four weeks because the persona, the scope, and the risk surface are all smaller.

How secure are banking chatbots?

As secure as the vendor architecture, the deployment configuration, and the prompt design make them — which is to say, secure when treated as a regulated system, risky when treated as a marketing widget. The non-negotiables are SOC 2 Type II, GDPR alignment (and CCPA in the US), encryption in transit and at rest, configurable data residency, conversation-level audit logs, and a written DPA. Beyond the vendor's posture, security depends on your prompt design (no fishing for PII), your scoping (no open-internet answers on regulated topics), and your monitoring (anomaly detection on conversation patterns).

Can banking chatbots replace human bankers?

No, and the banks that frame it that way usually fail. The model that works is "first line of triage." The bot resolves the volume intents — balance, statements, branch hours, card services, FAQ — so the human banker has time and context for the complex conversations: a mortgage modification, a small-business credit line, a complaint that needs empathy and judgment. The bot doesn't replace the banker; it lets the banker spend a Tuesday morning on three meaningful conversations instead of forty routine ones.

What's the average cost of deploying a banking chatbot?

It varies by an order of magnitude. A focused deployment on a SaaS platform like LiveChatAI or Intercom Fin can be live in four to six weeks with platform costs in the low five figures annually for a mid-sized bank. A tier-1 enterprise deployment with Kore.ai or a custom build can run into seven figures for the first year with implementation fees. The honest framing for a buying committee: pick the project's scope first, then the vendor whose pricing model matches that scope. Don't pick the vendor and then try to fit the scope to their pricing.

Further reading on AI chatbots and conversational AI:

Conversational AI in Financial Services: 6 Use Cases for 2026

25 Real-World Chatbot Use Cases Across Industries

6 Best Examples of Conversational AI in Different Industries

21 Chatbot Examples (2026): E-commerce, B2B & More

Top 12 Kore.ai Alternatives & Competitors

Omnichannel Chatbots in 2026: Features, Benefits & Use Cases